Партнерка на США и Канаду по недвижимости, выплаты в крипто

- 30% recurring commission

- Выплаты в USDT

- Вывод каждую неделю

- Комиссия до 5 лет за каждого referral

Central and South America

Mark Elliott

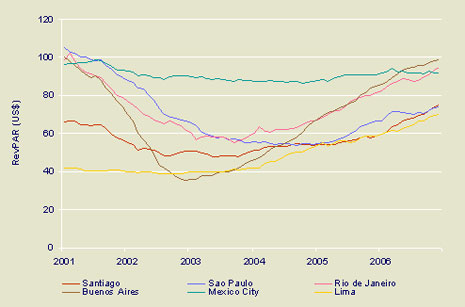

Will the real Latin America please step forward – in one corner, political instability, boom and bust economics and severe social problems, in the other, vibrant multi-ethnic cultures, cosmopolitan cities and unrivalled natural beauty. In 2006 the region was finally stepping out of the shadows of 2001-02. With both the Central American (+8.7%) and South American (+8.1%) regions exceeding the global average for tourist arrivals by some distance, the hospitality industry is happy. Investors’ confidence levels are also rising. South American nations are enjoying an influx of capital from Western Europe, while Central America is benefiting from its proximity to the USA, often in the form of large high-end projects such as golf resorts and residences. International hotel chains are also setting up home, with cities such as Buenos Aires, Caracas and Santiago seeing the supply of the four and five-star rooms swell. While no Latin American city makes the top 20 of the revPAR GRI, many cities are climbing back from their post-Millennium lows – as illustrated in the graph below. Only two cities – Santiago and Lima - have overtaken 2000 levels while other cities continue to move up the index. Rio de Janiero leads the region in 61st place, followed by Buenos Aires and Mexico City, at 62nd and 70th place respectively.

Argentina

Good exchange rates and a growth in tourists balanced out Argentina’s relatively minor social problems. Latest results from the World Tourism Organisation (UNWTO) confirm that international tourist arrivals were up 7.6% last year, continuing the upward trend since the political instability of 2002 and devaluation of the Peso. Most visitors come from the USA, Brazil or Chile, but a weak Peso is bringing in more people from the rest of Latin America and marketing aimed at China is widening Argentina’s appeal. With romantic images of Spanish colonial architecture, café culture, and street tango, the vibrant city of Buenos Aires is again capturing the imagination of tourists. In a response to increased demand, the hotel industry is dancing to the same tune. New developments in the four and five-star sector - including those from Hyatt, NH and Sol Melia – are boosting the city’s supply. MICE tourism is seeing strong growth as the government actively promotes this sector. Both average room rates and revPAR are up – 16.2% and 15.6% respectively - although occupancy has fallen slightly.

Brazil

With so much promise, but so many problems, Brazil has yet to fulfil its massive potential as a holiday destination – but there were signs of change in 2006. Stimulated by state investment in infrastructure and incentives targeted at developers, the government tourism body, Embratur, is encouraging hotel investment along Brazil’s north-eastern beach resorts. Embratur has also opened dedicated tourism offices in the US and major European cities in an attempt to drive up international arrivals to Brazil, which has traditionally relied on domestic tourism. While around 65m Brazilians holidayed at home in 2006, just 6m international visitors joined them. The importance of more tourists from overseas is clear – while domestic tourists embrace the low-cost culture initiated by GOL Airlines and Accor’s Formula 1 brand, international visitors are prepared to spend much more. The 6m international tourists spent around US$5 billion in Brazil – the same amount as the 65m domestic tourists. One long-term problem for Brazil has been its lack of air links with Europe, which is reflected in the low number of arrivals last year – 2.5m. However, new direct Lufthansa flights between Munich and Sao Paulo are having an impact. The airline, in combination with Swissair, now offers 19 direct flights to Brazil every week. The carnival capital of the world, Rio de Janeiro, is undoubtedly one of the world’s most beautiful cities. But Rio’s tourism is hampered by its reputation abroad, and the events of 2006 will not have helped. In terms of supply, Rio’s hotel industry remains fairly static. With the Ipanema and Copacabana districts already over-developed, there is little land left for construction. This maybe why average room rates have increased to just over US$155 in 2006, a rise of 12.7% from 2005, in turn driving revPAR. Occupancy levels are static at a little over 60%. The perennial bridesmaid in the battle with Rio for the hearts and minds of international visitors, Sao Paulo, performed well in 2006. Average room rates rose for the third consecutive year, to a five-year peak of US$124. Despite a drop in occupancy, this has boosted revPAR to just over US$74, a rise of 12%. Sao Paulo, as the main financial centre of Brazil and with excellent conference and exhibition facilities, is a magnet for MICE tourism. Although current hotel expansion and construction is dominated by the budget sector, recent openings, including the 123-room Marriott and 310-room Sonesta, have increased supply in the city’s luxury market.

Chile

Chile, the long sliver of land running down South America’s Pacific coast, has continued to punch well above its diminutive stature in 2006. Since the devaluation of the Argentinean Peso in 2002 – which severely dented Chile’s arrival figures – the government, along with the Corporacion Promocion Turistica (CPT) has been improving facilities to attract high-spending visitors. Aided by Chile’s national carrier LAN - the largest airline in Latin America - long haul arrivals from Europe, North America and, more recently, China rocketed to over 2.2m in 2006, according to the UNWTO. Economic stability, security, and a modern tourism infrastructure have all helped, as have Chile’s wide range of products - from ecotourism resorts in Patagonia, to skiing in new luxury centres close to Santiago. As the daily spend of long-haul visitor is nearly three times higher than short-haul, it is understandable that the CPT intend to expand this end of the market. The CPT expected international visitors to have generated around US$1.75 billion last year. As the central gateway city, Santiago is the hub of all Chilean tourism, and an increasingly important business centre. The boom of hotel construction in 2004 and 2005 - when five international brands were opened - created something of a price war. This calmed down in 2006, with average room rates rising to US$104, up 15.1%. Occupancy was up to 68.7% - reflecting Chile’s popularity.

Mexico

Hurricane Wilma wiped out the Gulf coast – the area that brings in 65% of the country’s revenue – and so the ongoing impact is harsh. 2006 was a year of restructuring, and visitor numbers fell by 2.8%. The Economist Intelligence Unit (EIU) estimates that some US$2.7billion has been pledged towards repairing the damage. The bulk of this money has come from private investors, but the Mexican government is putting in $250m. The political climate is stable, as presidential elections have come and gone without the economic shocks that have greeted previous voting, and hotel companies are delighted. Stable relationships with its US neighbour are also valued, as around 85% of visitors to Mexico cross the border from the US. New air routes between the two countries are encouraging more people to pay a visit, with low-cost airline Click Mexicana now flying direct between Cancun and Miami. Mexicana meanwhile has opened a Mexico City-Dallas route. The high-altitude capital of Mexico City enjoyed steady growth throughout 2006. Due to the dominance of business travel, occupancy reached 61.5%. The 0.7% increase in revPAR to US$92 was generated by a rise in average room rates, which now stand at US$149. Recent openings of a Crowne Plaza, NH Hotel and Holiday Inn have brought more rooms onto the market.

Peru

There’s no mystery behind the 2006 success of Peru - this intriguing land of the Incas. The Peruvian government has invested in a programme of sustained promotional activities, focusing on its nature tourism products. The country’s stand at the Hong Kong Travel Expo last year for instance, and an international advertising campaign, have brought in 10.7% more international arrivals. This growth is vital for the country, where tourism is estimated to account for 7.7% of total GDP. Peru’s gateway city, Lima, has performed well. The city has corrected its lack of first-class hotels recently, and the city’s revPAR improved accordingly. An occupancy-driven revPAR rise of 21.1% led to revPAR of US$49.

Summary on Central and South America

The region was set back by the hurricane and ongoing social unrest in some cities can still deter tourists from visiting. But there are some very positive signs. Relative economic stability, strong support from the government, and increased air routes will work together to increase its appeal. The bonus is the fact that many Latin American countries have been added to China’s list of authorised destinations, opening the region to a potentially huge flood of arrivals.

Central and South American cities revPAR Rolling-12 analysis (2001 – 2006)

HotelBenchmark™ Survey by Deloitte

The Middle East

Lorna Clarke, Dr. Costas Verginis

Middle East tourism gets set for takeoff

It is almost a tale of two regions. From the politician’s point of view, the Middle East dominates the agenda for all the wrong reasons – the Iraqi insurgents, tension between Israel and Lebanon, concern over Iran’s nuclear threat, and the continuing terrorist attacks.

But from the tourism industry’s perspective – the Middle East is the outstanding success of the decade. During 2006, travel and tourism is expected to have generated around US$148 billion, a figure that could double in the next ten years.

Even with the current backdrop of political unrest, destinations in the Middle East are developing at a phenomenal rate and now attract around 5% of the world’s tourists, making this the fourth most visited region in the world.

Massive investment in hotels, resorts, air travel and sports facilities have put other regions in the shade, and there is no shortage of funds as the Gulf States continue to diversify their economies. Tourism now rivals the traditional industries of oil and gas, and many countries are pursuing aggressive growth strategies.

Fastest on earth

The economic outlook for the Middle East as a whole is way ahead of the rest of the world, and hotels are being completed at breakneck speed to accommodate the expected influx of visitors. Dubai is the undisputed powerhouse of the region and home to some of the world’s tallest, largest and most opulent developments. It is said to be the fastest growing place on earth and, with a budget surplus of US$1.58 billion in 2005, there is plenty of cash to support the Emirate’s expansion plans.

Although Dubai currently looks like one big construction site, its popularity is astounding. More than 6 million visitors poured in during 2005 – doubling the number of tourists in just six years – attracted by year-round sunshine, key conferences including CITEX and Cityspace and massive shopping malls. The UK is the largest source market, with Europe as a whole accounting for nearly a third of all arrivals.

Dubai’s strategy is also to maximise the tourism potential of world-class sport. Having staged the world’s wealthiest equestrian event – the Dubai Cup – for some time, it now hosts the Dubai Tennis Championship, the Desert Classic Golf Tournament and, more traditionally for a Gulf State, camel racing. Ski Dubai opened in 2005, enabling people to enjoy winter sports while, outside, other holiday-makers swelter in the sun.

The Dubailand development will include the worldis first purpose-built sports city, covering 50 million square feet. This will include a golf course, a sports academy and a residential community – with the entire development set for completion by 2010. With so much to offer, itis not surprising that according to the HotelBenchmarko Survey by Deloitte for the first ten months of 2006, Dubai was the top performing Middle Eastern market in terms of both hotel occupancy and average room rates. At US$237, average room rates in Dubai are among the highest in the world, bypassing other first-class destinations such as New York, London and Paris.

Some analysts suggest Dubaiis hotel market is overheating, but with government plans to drive up tourist numbers from 6 million in 2006 to 15 million by 2010, hotel performance in Dubai will continue to do well. However, with more than 55,000 rooms predicted to enter the four and five-star market in the United Arab Emirates (UAE) over the next five years, the rate of growth may be restrained.

Neighbouring countries, like Qatar and Abu Dhabi, are keen to emulate Dubai and multimillion dollar projects are changing the Gulf landscape forever.

The makeover of Abu Dhabi is moving ahead quickly. The country now has its own airline – Etihad Airways – its own tourism board and many new hotels. In the first ten months of 2006, Abu Dhabi recorded the highest growth in average room rates across the region, up 47.6% to US$158, helped by several major exhibitions and conferences.

Bahrain has basked in the glory of Formula One Grand Prix, bringing in thousands of spectators to this small island, while enjoying the attention of millions of TV viewers. However, 2006 gave Doha the chance to shine, as the country hosted the Asian Games in December – second only to the Olympics in terms of global multisports events.

Investment is being been pumped into airport expansions and new aircraft, especially by Qatar Airways, which is now one of the fastest-growing in the world. Qatar also invested heavily to bring its roads, hotels and leisure facilities up to international standards for the Asian Games in December 2006.

In the firing line

The two countries caught in the firing line of Middle East politics are Lebanon and Egypt. Lebanon, having pulled itself together after years of civil unrest, had been making solid progress until its Prime Minister was assassinatedin February 2005. That year, visitor numbers went down by 10% to 1.2 million.

The future looked more positive in 2006, with 49% more tourists arriving during the first six months of the year. However, the picture changed in mid-July, when the capture of two Israeli soldiers by Hezbollah led to a devastating response from Israel. A review of hotel performance based on figures from Daily HotelBenchmarko by Deloitte shows that during the first three weeks of the crisis, Beirut hoteliers saw occupancy fall to around 33% – some 40% below the levels achieved in 2005. Rates remained fairly stable during the first week of the conflict; however these subsequently fell by over 30% in the second and third week, resulting in revenue per available room (revPAR) falling to just under US$40.

Despite this, the net impact on the city for the first ten months of 2006 was negligible. Although average room rates in Beirut dropped 5.2% to US$137 compared to 2005, occupancy managed to increase slightly to 51%. This reinforces the belief that as tourists become more resilient, the impact of such events is increasingly becoming relatively localised and short-lived. Egypt’s image was damaged through a series of bombings at popular resorts, but tourists are not easily put off. The country hopes to bring in 16 million international visitors by 2014. It is also appealing to Arab tourists and its Nawart Masr – ‘You light up Egypt’ – campaign is expected to drive Middle Eastern holiday-makers numbers up by 30%.

The world’s best

Hotels in the region enjoy some of the world’s highest occupancy and average room rates. For example, in 2005, the Middle East region saw revPAR increase 21.4%, helped by an incredible 22.8% increase in average room rates – up to US$117 compared to US$95 in 2004.

Looking at the first ten months of 2006, revPAR was up 14.5% compared to the same period last year. Although continuing terrorist threats in key areas combined with an increase in hotel supply has seen occupancy fall 2.0% for the first ten months of 2006, average room rate growth remains strong. This surged 16.8% to US$131, and the resulting US$89 revPAR puts the Middle East just behind Europe.

Room for development

A number of international hotel chains have rapid expansion plans for the Middle East, including Accor, which hopes to increase its portfolio of 18 hotels to 58 by the end of 2009. Marriott International is planning a 250% increase in its rooms over the next five years, while Movenpick Hotels and Resorts will add 13 properties by 2008.

Millennium Hotels and Resorts has opened regional headquarters in Abu Dhabi to oversee the development of 35 hotels in the Middle East and North Africa over the next five years. Hilton Hotels Corporation and Four Seasons Hotels and Resorts are also expanding fast.

Although international operators tend to dominate, local operators are also staking their claims. Aldar Properties is planning 32 hotels in Abu Dhabi within the next three to seven years, ranging from small boutique accommodation to major resorts.

Emirates Hotels & Resorts is building a US$490 million 77-storey hotel in Dubai’s Business Bay area. The Emirates Park Towers Hotel and Spa, the group’s fifth property, scheduled for completion in 2010, will have 900 rooms and 300 serviced apartments.

To date, most hotel development has focused on the luxury end of the market but the gap in the budget sector will soon be filled. easyHotel has signed a deal with Dubai-based investment company, Istithmar, to bring 38 budget hotels into the Middle East, North Africa, India and Pakistan by 2011.

Yotel, a revolutionary hotel concept inspired by Japanese pod hotels and business class air travel, will also challenge the status quo. Its first hotels in London’s two main airports, Heathrow and Gatwick, will soon be followed by others in the Middle East.

Whitbread Plc, one of the UK’s leading hospitality companies, plans to bring its Premier Travel Inn brand into the Middle East. Initial sites will be in Dubai, adding 800 rooms for the business traveller. The first Premier Travel Inn scheduled to open is the 300-room hotel at Dubai Investment Park in the final quarter of 2007.

InterContinental Hotels Group will join the budget market push in 2007, when the first Express by Holiday Inn opens at Knowledge Village in Dubai with 240 rooms. The group has plans for around 20 properties in the Gulf and 20 more in Lebanon and Syria.

Going large

At the high end of the spectrum, the development pipeline boasts schemes that will enhance the Middle East’s image as a place where fantasy meets reality.

For instance, real estate developer Nakheel has teamed up with US developer Donald Trump to create a centrepiece for the Palm Jumeirah. Located on the ‘trunk’ of the palm, the 48-storey Trump International Hotel and Tower will comprise a 300-room condo hotel, 360 freehold residential apartments, offices, restaurants, business centres, health clubs, swimming pools and entertainment venues.

Dubai already has the world’s tallest tower, largest shopping mall and many other projects described in the superlative, and now it will boast the world’s largest hotel. With 6,500 rooms, the Asia-Asia hotel will be the centrepiece of a US$27.3 billion tourist and leisure resort located in Dubailand.

Not to be outdone, Abu Dhabi is pushing ahead with its Emirates Pearl Island project, plus another US$27 billion island development. This will create an island half the size of Bermuda, with 29 hotels, including one with a 7-star rating. It will be developed in three stages between now and 2018 and will eventually become home to 150,000 residents.

In Oman, The Wave is being built on reclaimed land along the Seeb seafront. This US$800 million resort will stretch along 7.3km of beachfront west of Muscat and is due to open in 2009.

By the plane load

Passenger traffic is growing faster in the Middle East than anywhere else in the world – up 15% in 2005, according to the International Air Transport Association. All the major airports are being upgraded, and regional carriers are placing multibillion-dollar orders to expand their fleets.

Over the next 20 years, Middle East airlines are expected to buy around 870 aircraft worth US$115 billion. In 2005, Emirates Airlines placed the biggest order Boeing has ever received for 42 Boeing 777s, worth US$9.7 billion. Qatar Airways, with a current fleet of 45 all-Airbus aircraft will soon include 60 generation Airbus A350s as well. The airline will be among the first to fly the innovative twin deck A380 super jumbos.

Sustainable growth

The World Tourism Organisation predicts the region will see an average annual growth rate of 6.7% – the highest in the world – leading to around 68.5 million international visitor arrivals by 2020.

But this incredible transformation of the region comes at a cost to the environment, and the global tourism industry is beginning to question whether the current level of growth makes sense and is sustainable.

Some experts are calling for immediate action to preserve the region’s ecology, and many developers are adopting high standards to protect and conserve the natural environment. Nakheel, for example, has invested in more than 20 research projects to promote environmental sustainability. Marine regeneration has created a new ecosystem on The Palm, while the shelter of the breakwater provides a fertile habitat for coral to grow. There is also the pressing issue of recruitment, as the demand for trained staff increases. Concerns are likely to escalate, because many of the hotels and resorts are huge multimillion-dollar schemes, needing thousands of staff to look after guests and run the business.

For example, the 300 room Emirates Palace in Abu Dhabi has more than 1,000 staff. Acquiring, developing and retaining staff will

therefore be a major challenge, and one that will be exacerbated by the fact that the traditional Indian workforce may prefer to return to their own country, where the hotel sector is also booming.

Putting these two issues to one side, the sun will undoubtedly continue to shine in the Middle East and despite the shifting political landscape tourism is likely to remain big business.

HotelBenchmark™ Survey by Deloitte

From no-go zone to must-see destination: how a region was reborn

Annabelle Thorpe

Once regarded as a dangerous no-go zone, the Middle East is emerging as the hottest travel destination of the year. While many countries are seeing visitor numbers fall as the recession continues to bite, the Middle East is bucking the trend, with big increases in numbers of tourists, alongside major investment in new hotels, attractions and tours.

"The Middle East is our biggest selling region by far this year," says Mark Stacey, middle east product manager for Cox & Kings. "Across the region, sales are up about 35% - and that's after a 38% rise in 2008. Syria has gone through the roof." Stacey believes that the constant news focus on the Middle East has brought countries such as Jordan, Syria and Iran to the forefront of people's minds. "These countries have had a high profile in recent years - even if not always for positive reasons - and I think that arouses people's curiosity," he says.

Though political tensions remain, in particular between the Iranian and British governments, the Foreign Office no longer warns tourists against travelling to the Middle East, except for a few specific areas such as Iran's border with Iraq.

"It's definitely about the law of the neighbouring destination," says Tom Barber, founder of Original Travel, which specialises in the Middle East. "Dubai became very popular and then people started looking over the border into Oman and wondering what that was like.

"Likewise Jordan's popularity has been to Syria's benefit. Every Middle Eastern destination we have added has tripled in demand in the first couple of years." Mainstream tour operators are also profiting from the boom: Thomson has seen an 11% rise in bookings to Egypt this summer, and is expanding its programme for 2010, introducing a new resort, Marsa Matruh, on the Mediterranean coast.

But independent travel is becoming increasingly easy too, thanks to new flights and rail services and improved infrastructure. BMI () increased its routes to the Middle East in May, and now offers 10 flights a week between Heathrow and Amman and Heathrow and Beirut, as well as regular flights to Jeddah, Damascus and Doha.

"Self-drive is booming in Jordan," says Julie Kemp of the Jordan Tourist Board. "It's very easy to navigate, with only three main roads traversing the country and accessing all major sites."

Syria is one of the biggest winners: visitor numbers were up 15 per cent last year on 2007, and almost $6bn of tourism development is under way.

But it could still be eclipsed by Lebanon. The New York Times put Beirut at number one in its list of places to visit for 2009, and the much-awaited opening of Le Gray hotel next month looks set to re-establish the city as a party capital. Explore (explore. co. uk) has added extra dates for its Lebanon tours after existing trips sold out.

"People are looking to stretch their boundaries," says Mark Stacey at Cox & Kings, "and the Middle East is the obvious option. It feels a little bit edgy, even though it's a very safe place. It's a winning combination."

The Observer, 2009

Western Europe

Clouds over the Mediterranean

The recession clobbers one of Europe’s biggest industries

How badly is the recession hurting Europe’s tourism industry during the all-important summer holidays? The outlook is grim, judging by the trend set earlier in the year. After slipping in the second half of 2008, passenger numbers in Italian airports fell by 13.4% in the first quarter of this year. Spain recorded a similar fall between January and June, with airports on Lanzarote (down 19.1%) and Tenerife (down 17.8%), two popular holiday islands, losing more than most. The French Riviera is suffering, too: Nice airport reported a drop of 8% in passengers during the first half of the year. Firms have slashed travel budgets, families are spending less on leisure and Europe’s airports are feeling the pain.

For hotels as well, the recession is biting in France, Spain and Italy, Europe’s biggest holiday destinations. During the first five months of the year, the number of overnight stays by foreign visitors in French hotels fell by 15.5%. The number of foreigners who visited Spain in the first six months was 11.4% lower than in 2008. The situation is equally grim in Italy, where overnight stays by foreign guests were 11.5% lower in the first half of the year. Bernabo Bocca, chairman of the Italian hoteliers’ association, described the results as a debacle.

Many jobs are at risk. In 2007, before the recession struck, France boasted nearly 200,000 hotels, pensions, campsites, restaurants, cafés and travel agencies, which employed almost 900,000 people on average during the year and took in some €70 billion ($96 billion). Spain had about 293,000 firms, with 1.4m employees and a turnover of €80 billion. Around 270,000 firms work in tourism in Italy and Mr Bocca says the 15% drop in turnover expected this year will quickly lead to job losses. Rome’s hoteliers’ association fears its members will shed 10,000 jobs this year.

Italy has beaches, mountains and lakes, and claims more artistic treasures than any other country. But last year 7.4% fewer people visited the Doge’s palace in Venice than in 2007, and attendance was down by 3.8% at Florence’s Uffizi gallery and 12.4% at Pompeii. Yet some attractions hold their own. Disneyland Paris, Europe’s biggest crowd-puller with 15.3m visitors in the year to last September, reported a slight pick-up in the next six months. But that was something of a pyrrhic victory. Occupancy at the park’s hotels was 2.7 percentage points lower, average spending by visitors fell by 3.7% and revenues by 7.3%. At museums, resorts and theme parks, expectations for this year and next are generally poor.

The euro’s strength against the pound and the dollar adds to the problems of European tourism’s big three. Britain sends more tourists to Spain than any other country, but the 6.1m that arrived between January and June were 16% fewer than during the same period of 2008. British and American tourists are the most numerous guests at expensive hotels in particular, so the luxury hoteliers of Paris and Rome are feeling their absence.

Mauro Cutrufo, Rome’s head of tourism, believes the recession is an opportunity to push grandiose new schemes: marinas to match Monte Carlo, golf courses like those in Spain and theme parks to rival Disneyland. That is probably a mistake. However the world’s economy fares, tourists are unlikely to abandon Mickey Mouse in favour of a Roman theme park. But foreigners will always want to visit the Colosseum and the Vatican museums, or make a pilgrimage to Paris to see the Mona Lisa.

The Economist, 2009

Spanish tourism feels pinch of economic downturn

Benalmádena, Spain – Few Spaniards would sacrifice their annual summer vacation. But while Spain's beaches are still busy, shops and restaurants at its resorts are ominously quiet as the country's economic crisis envelops the tourism industry.

After 50 years of uninterrupted growth, Spain's overbuilt and relatively expensive resorts seem ill-placed to cope with a downturn, at a time of increasing competition from cheaper, less-crowded destinations like Croatia and Turkey.

"In 48 years, I have never seen losses like this; tourism bosses I'm talking to have never suffered so much," said Domenec Biosca, president of Spain's Association of Tourism Directors and Experts.

He said that in many parts of the country, tourism was already in deep recession, as both Spaniards and foreigners travel less distance, stay less time and spend less money.

Spain's biggest hotel group, Sol Melia, reported that profits fell 41 percent in the first half of the year, while those at business hotel group NH dropped 20 percent.

Revenues in the Canary and Balearic islands have fallen as much as 12 percent this year, Biosca estimated, predicting that such mature destinations would gradually decline in the face of foreign competition, despite lowering their prices.

Benalmádena, a resort near the southern city of Málaga, is one such mature destination.

Its wide strip of golden sand is shadowed by 1970s hotels, high-rise apartments and cul-de-sacs of whitewashed houses that stretch in a 50-kilometer, or about 30-mile, swath of concrete from Málaga in the east to Marbella in the west.

While the town's beach was packed with sunbathers on a typical afternoon in late August, despite the explosion of a small bomb by the Basque separatist group ETA on Aug. 17, local businesses said sales were down.

British and Spanish tourists strolled past Hami Bhot's beachwear store, but only a few entered and fewer still spent any money. Takings have halved this summer, he said.

"I can perhaps survive another year but then I will have to close. Maybe I will go back to India; the economy is better there," said Bhot, who had dimmed the shop's lights to save money.

Tourism, which accounts for up to 15 percent of Spain's gross domestic product and one in seven jobs, is suffering just as the economy needs it to take up the slack left by the rapidly contracting construction sector.

Until recently, towns on Spain's coasts relied on construction for most of their income and growth, but as foreign home buyers shun Spain, these towns can ill afford to lose tourism revenues as well.

For the first time in a generation, Spaniards have had to slash spending on things like vacations as their incomes stagnate, prices rise and credit dries up. Unemployment, which leapt by more than 100,000 in August to a 10-year high of 2.5 million, has become a major concern for the first time in years.

Spain was the world's No. 2 tourist destination after France last year, with almost half of its 60 million foreign visitors coming from Britain and Germany.

But both countries are teetering on the edge of recession, and the British are turning away from euro-denominated countries like Spain after the British pound's 15 percent slide against the euro in the last 12 months.

Britain's Thomas Cook, Europe's second-largest travel company, has cut destinations in euro-zone countries and boosted offerings to Egypt and Turkey, which received 25 and 15 percent more tourists last year, respectively.

Eight percent fewer foreigners arrived in Spain this July, according to Ramón Estalella, secretary general of the hotel confederation Cehat. But more worrying, he said, will be the impact of Britain's economic plight on bookings for later this year.

"Most package holidays in Britain were sold between January and April, when there wasn't this feeling of recession as there is at the moment," Estalella said. "I'm much more worried about bookings being made right now for the winter season."

But it is economic pain in Spain, contending with the end of a 10-year-long property boom, that poses the greatest threat to the tourism sector, experts say.

Hotel occupancy in some northern areas favored by Spaniards fell a hefty 15 percentage points over the summer, said Estalella, compared with a 3- to 4-point drop across the country.

Establishments reported a respectable 85 percent occupancy rate in August, Estalella said, but to achieve that they resorted to price freezes and special offers that kept the average hotel bill increase to just 2 percent.

The crash of a plane carrying tourists from Madrid to the Canary Islands on Aug. 20, killing 154 people, was another potential damper on the sector.

In Benalmádena, hoteliers and apartment owners reported that, for the first time, many guests had cut their stay to one week from two. Others are coming just for a long weekend.

New York Times, 2009

Spain: Madrid

Nina Bruun

Good things are said to come in threes, and this is certainly the case for hoteliers in Madrid. Firstly, the city is flourishing as a venue for international conferences, secondly, the country’s economy is outpacing the rest of the European Union (EU); and thirdly, Madrid airport’s beautifully designed new terminal has doubled passenger capacity.

The combination of these three factors helped give Madrid hoteliers solid revenue per available (revPAR) growth over the last year up 7.0% to €80 according to latest data from the HotelBenchmark™ Survey by Deloitte.

Hotel performance back on track

The last twelve months have been great for hoteliers in Madrid with revPAR growth nearly doubling compared to the same period the previous year. This is a stark contrast to the two years of revPAR declines in 2003 and 2004. Occupancy dropped as low as 64% in the twelve months to March 2005 but is now back to 70%. One of the main reasons for this has been improved business performance with a number of organisations choosing to locate major conferences and events in the city.

Comparing the seven cities tracked by the Spanish edition of the HotelBenchmark™ Survey, Madrid is only beaten by Barcelona in terms of absolute revPAR as seen in the table below. Although the occupancy levels of both cities are nearly the same, Madrid still achieves lower average room rates than Barcelona. Valencia has seen the highest revPAR growth of any market benefiting from events leading up to the America’s Cup which takes place in June and July 2007. This has helped hoteliers push up average room rates from €65 to €73 in the last twelve months.

Spanish city performance – twelve months to March 2007

Occupancy (%) | Average Room Rate (€) | RevPAR (€) | |||||||

Apr 06 - | Apr 05 - | % Change | Apr 06 - | Apr 05 - | % Change | Apr 06 - | Apr 05 - | % Change | |

All Spain | 66.1 | 65.8 | 0.5 | 85 | 81 | 5.7 | 56 | 53 | 6.2 |

Alicante | 58.1 | 66.1 | -12.1 | 67 | 64 | 5.5 | 39 | 42 | -7.3 |

Barcelona | 70.8 | 69.8 | 1.5 | 129 | 122 | 5.5 | 91 | 85 | 7.1 |

Bilbao | 66.9 | 68.7 | -2.5 | 72 | 68 | 7.0 | 48 | 46 | 4.2 |

Madrid | 70.2 | 68.7 | 2.1 | 114 | 108 | 4.8 | 80 | 75 | 7.0 |

Seville | 63.7 | 62.6 | 1.8 | 94 | 88 | 6.1 | 60 | 55 | 8.0 |

Valencia | 67.1 | 65.0 | 3.4 | 73 | 65 | 12.1 | 49 | 42 | 15.8 |

Zaragoza | 74.7 | 71.8 | 4.0 | 71 | 66 | 7.3 | 53 | 47 | 11.5 |

Conference choice

Madrid is now the 19th most popular worldwide conference destination, according to the International Congress & Convention Association (ICCA), and several major events have been were staged in the city over the last year. June 2006 was particularly busy, with more than one 1m people attending the ten day biennial Madrid International Motor Show.

In the same month there were several medical conferences, as well as the biennial TEM International Municipal Services and Equipment Trade Fair. As a result, Madrid’s hoteliers saw the highest average room rates of the year, at €124. Other key events that helped boost numbers during the year included Construtec (construction industry), Expodental (dentistry) and Veteco (windows). 2007 has already seen a number of trade fairs including Climatización (air conditioning), Genera (international energy and environment) and Intersicop (bakery).

While hotel operators are delighted with these extra business visitors, Madrid’s Tourist Board has plans to widen the city’s appeal still further. It is now focusing on the nightlife and cultural attractions to bring in more leisure travellers.

Economic boost for now

In addition to attracting events to the city, Madrid is benefiting from the strength of the Spanish economy, which grew by 3.9% in 2006 according to the Economist Intelligence Unit (EIU). This was above the European Union average of 2.8% and boosted Madrid’s performance as the centre of the country’s commercial activities.

However looking ahead, the EIU expects Spain’s pace of economic growth to slow to 3% in 2007 and to 2.2% in 2008 driven by more moderate domestic demand. There are concerns that the 14 year property boom that has put Spain near the top of the euro zone’s growth league is coming to an end. House prices have climbed 180% in the past decade - more than doubling in real terms.

In addition, inflation rates above the euro area average have also had an impact on the country’s loss of competitiveness. This is coupled with high levels of personal borrowing which have climbed to more than 110% of income and left more than half of Spain’s population with difficulties meeting their monthly loan repayments - according to the Bank of Spain. With this in mind, economists believe more difficult conditions lie ahead for Spain and that the country must diversify its economy to avoid over-reliance on the construction industry and prevent a further slowdown in the years to come.

Meanwhile, several hotels have opened during the last year, confirming Madrid’s continuing popularity with investors. These include the 158-room Hesperia Emperatriz, the 260-room Husa Paseo del Arte and the 108-room Barcelo Torre Arias among others. More will open in 2007, including the Express by Holiday Inn Barajas, the Hilton Madrid Airport, the AC Mostoles and the NH Fuenlabrada. This planned new supply will add more than 600 additional hotel rooms to the market.

A major hub

Madrid now has one of the world’s largest and most modern airports with the opening of the new €670m terminal at Madrid Barajas in February 2006. This has doubled passenger capacity to 70m a year, making the airport a major hub for flights between Europe and Latin America.

This fourth terminal adds two buildings, two runways, extra shopping and leisure facilities. The airport can now handle 120 aircraft movements an hour, up from only 78 previously. Its design has attracted the attention of RIBA, the Royal Institute of British Architects, who – in association with the Architects’ Journal – presented the airport with its annual Stirling Prize in October 2006.

Passenger arrivals to Madrid compared to revPAR 2

It is interesting to compare Madrid’s passenger arrivals with revPAR growth, as shown in the graph above. Until mid-2002, the two follow the same pattern, but then passenger numbers recover much quicker than revPAR. Whilst passenger numbers recovered, revPAR continued to fall as the city struggled to absorb new supply. Between 2000 and 2003 Madrid saw the opening of some 40 hotels which put pressure on both average room rates and occupancy. This fall was further exacerbated not only by the weak global economy at the time but also by the fact that passengers used Madrid as a hub on their way to other destinations.

Que sera, sera?

Overall, the last year has been a good one for hoteliers in Madrid and the outlook for the rest of 2007 continues to look promising. Spain’s economy is expected to grow 3% - ahead of the rest of Europe - and despite gloomy predictions about house prices, early findings from the HotelBenchmark™ Survey show revPAR up almost 10% in the first quarter of 2007 alone. Even though extra hotel rooms are coming onto the market, we expect domestic and international demand for accommodation to stay strong.

HotelBenchmark™ Survey by Deloitte

Germany

Konstanze Auerheimer

German hoteliers report revPAR growth for the second consecutive year

After an impressive 4.7% increase in revenue per available room (revPAR) during 2004, German hoteliers had high expectations for 2005. However, year end results from the HotelBenchmark™ Survey by Deloitte reveal that hotel performance slowed markedly during 2005. RevPAR grew only marginally, up 1.6%, with average room rate declines being offset by an improvement in occupancy. However, 2006 is the start of an exciting year for the tourism industry in Germany. Prospects look bright as the country is buzzing with the anticipation of the FIFA World Cup and the hotel industry is gearing up to welcome its first football fans. However, what remains to be seen is how hoteliers will really score at the final whistle.

Below average revPAR growth

At 1.6%, Germany’s revPAR growth in 2005 lagged behind the European average of 4.3%. Whilst across the whole of Europe both occupancy and average room rate growth fuelled the increase in revPAR, the major Western European economies all experienced very different performances. In Germany the 2.4% increase in occupancy was very impressive, especially coming on the back of a 4.3% rise in 2004, however at 61.5% German hotels still achieve the lowest occupancy of any of the major European countries. This combined with a fall in average room rates of 0.8%, (as hoteliers struggled to maintain the growth that they had experienced in 2004), resulted in German hotels achieving a revPAR of just €50, the lowest revPAR across Europe. Like Germany, hotels in Spain also suffered from a fall in average room rates of 0.5%, and this combined with only a marginal increase in occupancy of 1.6% left revPAR up just 1.1%. Conversely, hotels in the UK experienced a 3.3% improvement in average room rates – in part due to the preferential exchange rates – but this was curtailed by 0.5% decline in occupancy. The UK was the only country in Western Europe to report a decline in occupancy primarily due to loss demand in London following the July 7th bombings.

Economic growth continues

Gross Domestic Product (GDP) continued to grow in 2005 for the second consecutive year, mirroring the trend in revPAR growth. However, at 0.9% GDP growth was nearly half that achieved in 2004, when the economy grew 1.6%. Although exports remain the main driver of economic growth in Germany, improvements in consumer and business sentiment and increasing domestic demand are all helping the economy recover. Short term prospects according to the Economist Intelligence Unit (EIU) look positive with GDP estimated to grow by 1.7% in 2006 and 2007. However, there remains one cloud on the horizon for 2007 as the newly elected German government have agreed to increase the country’s value added tax from 16% to 19%. By taking this step, alongside additional reforms and public spending consolidation, the government hopes to regain the Germany’s position as one of the top three European nations by 2015.

Improving tourist numbers

Tourism numbers are also continuing to improve across Germany. Preliminary numbers from the World Tourism Organisation (UNWTO) estimate that international visitor arrivals increased 6.5% in the year-to-November compared to the same period in 2004. This is better than the European average, which UNWTO estimate is 4.3%. Furthermore, data from Destatis, the German statistics office, reveals that domestic and foreign overnight stays grew by 1% and 6% respectively resulting in total overnight stays of 344m. It is encouraging to see that domestic demand, which accounts for over 86% of the overnight stays, grew in 2005 after declining in 2004.

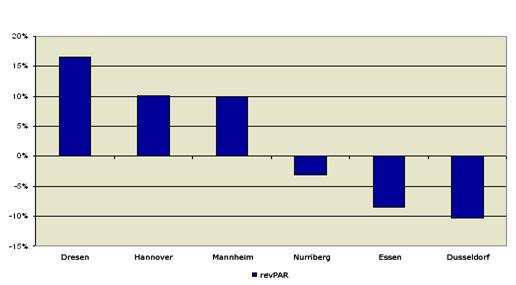

Mainly positive results for German cities

Of the 21 cities tracked by the German edition of the HotelBenchmark™ Survey five markets experienced revPAR declines in 2005. Berlin, Düsseldorf, Essen, Munich and Nuremberg all performed below 2004 levels. As can be seen in the graph below, the top three performing cities in 2005 were Dresden, Hannover and Mannheim. A number of visitors were attracted to Dresden in February to mark the 60th anniversary of Dresden’s destruction during the Second World War. Then in October the famous Frauenkirche (the city’s church) was re-opened having been restored to its former glory. Whilst 2005 was a favourable trade fair year for hotels in Hannover, the biennial trade fair cycle affected hotel performance in Essen and Düsseldorf where revPAR declined compared to 2004. Both cities had an excellent April with the Interpack fair; however this could not offset the declines in March, May and October. Events such as the Drupa – Print Media Fair which take place every four years and the triennial K-International Fair were not held in 2005.

Welcomed World Cup boost

Despite the challenges faced by German hoteliers in 2005, the FIFA World Cup, being hosted by the country this summer could finally bring a smile to their faces. The German tourist board (DZT) estimates the country will benefit from 5m additional overnight stays from the 10m visitors attending the championship. The FIFA World Cup will run from 9 June to 9 July. The games will be played across 12 cities - kicking off with the first match in Munich and Berlin will host the final. In addition, each national team plus their representatives have chosen a home base from 12 cities. Cologne will welcome Brazil, Dusseldorf will host the Mexican team and Argentina will stay in Frankfurt. The ‘World will be welcomed as friends’ is the German motto for the World Cup. Currently the World Cup Accommodation Service (WCAS) is predicting that average room rates will reach €185 (including tax) and that occupancy levels will be between 70-80% during the four weeks of the tournament. WCAS assists fans with booking hotel accommodation and had taken allocations at 550 hotels. Currently, around 38% of WCAS room allocations are reserved. The remaining rooms were returned to hoteliers at the end of February for them to market.

And the winner is…

The FIFA World Cup will focus the world’s attention on Germany. Whilst the country is expected to benefit from increasing visitor numbers and a boost to the tourism industry, German hoteliers should experience impressive growth in performance during the four weeks of the tournament. Daily HotelBenchmark™, will be monitoring how each of the cities fares during the World Cup. The German hotel association (Hotelverband Deutschland IHA) predicts a 3% growth in occupancy with a slight increase in average room rates in 2006. With economic fundamentals like GDP growth and consumer confidence moving upwards, 2006 looks set to be an important year for German hoteliers. However, we will have to wait until the whistle is blown for full time at the end of the year to see what really happens to the hotel industry.

Key European countries – revPAR percentage change 2005 vs. 2004

Germany’s winners and losers – revPAR percentage change 2005 vs. 2004

Note: All analysis in Euros.

HotelBenchmark™ Survey by Deloitte

Berlin tourism passes its peak

Recent years saw Berlin emerge as the third most-visited tourist destination in the EU after London and Paris. But its new-found popularity is still far from guaranteed, with visitor numbers starting to flag.

The statistics presented in August by Berlin's Tourism Organization were disappointing. For the first time since 2003, the number of domestic visitors staying overnight in Berlin fell.

And these are the visitors that matter. 61 percent of tourists in Berlin are domestic visitors, so even an undented flow of foreign visitors fails to compensate for their shrinking presence.

In fact, even while this 40 percent share of hauptstadt tourism shows no signs of declining, profile is changing: While British, Italian, Dutch, Spanish and US tourists are still flocking to the German capital, Asian visitors are less keen they once were. Statistics show a 25 percent drop in the number of Chinese and Japanese tourists staying in Berlin.

A dull year

But Hanns Peter Nerger, manager of Berlin Tourismus Marketing, is still far from pessimistic.

He puts the 2008 slump down to the year's lack of major, crowd-pulling events on a par with the 2006 World Cup – a highlight which triggered a tourist boom felt even in 2007 – the Knut sensation of summer 2007, or the enormously popular Moma exhibition in 2004.

2009, he insists, will be different, what with the athletics world championships, the 20th anniversary of the fall of the Berlin wall and the festivities surrounding the 60th anniversary of the Federal Republic of Germany.

Economic blues

But overall, the experts agree that the new figures are not Berlin-specific. The downwards trend more likely reflects a general economic unease, while spiraling living and fuel costs have left many thinking twice about the city-breaks they took for granted a few years ago.

The German Airlines Association say that rising fuel costs are expected to lead to a 5 to 7 percent drop in demand, with average prices rising by up to 20 percent.

"Berlin airports might be growing faster than the average German airport," said CEO of Berlin Airports Rainer Schwarz, "but we still expect reduced growth for the second half of the year."

Burkhard Kieker, soon to replace Hanns Peter Nerger as manager of Berlin Tourismus Marketing, agrees that Berlin's current dry patch in terms of tourism is down to the end of the low-cost flying era.

"In Berlin, there is a close correlation between tourism and air travel," he told Berlin daily taz. "In recent years air traffic here developed twice as fast as it did in other European airports. That has to do with the hype surrounding Berlin but also vast array of low-cost airlines. But obviously no one spends a month of their summer holidays in a city, and Berlin was always people's second holiday. So when people are tightening their belts because of the rise in fuel costs, the first thing they do is cancel their trip to Berlin."

eTurboNews: Global Travel Industry News, 2009

Eastern Europe

Eastern Europe – a key growth market for the global Travel and Tourism industry

Leonie Tait

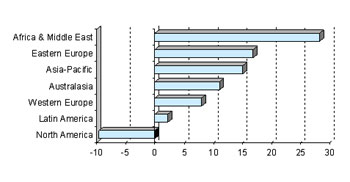

Eastern Europe offers the global travel and tourism industry a golden opportunity for growth, according to the latest research from Euromonitor International.

Between 1999 and 2003, Euromonitor found that Eastern Europe was the only region to record consistent annual growth in terms of incoming tourism. This growth rate of approximately 17% was well ahead of more developed regions such as Western Europe and North America.

Growth in international tourism arrivals by region

Serbia and Montenegro drives growth in the region

Serbia and Montenegro spearheaded growth in the region. This former Yugoslav State witnessed dramatic growth, with incoming tourism increasing by some 207% between 1999 and 2003, although this was from a small base of just in 1999. Other Eastern European destinations including Croatia, Latvia and the Ukraine also featured highly in Euromonitor’s growth rankings.

Economic stabilisation in Eastern Europe benefits tourism

Euromonitor International’s research suggests that this dynamic growth in Eastern Europe is the result of a convergence of several market factors. Of primary importance has been the stabilisation of economic conditions in Eastern Europe, which has allowed for government investment in infrastructure and the tourism industry itself.

The inclusion of several Eastern European countries in the EU in May 2004 has created new opportunities for trade and investment. EU membership is expected to have a positive impact on growth prospects in the new Member States, which include the Eastern European countries of Poland, Hungary, the Czech Republic, Slovenia, Slovakia, Estonia, Latvia and Lithuania. These countries will receive the benefit of the EU Structural and Cohesion Funds if they manage to maintain a stable macroeconomic environment and institutional and microeconomic structures that are conducive to growth. The result will be greater economic stability in the region and more money to inject into tourism.

Budget airlines attract tourism to Eastern Europe

Eastern Europe has recently been opened up to low cost airlines, such as Sky Europe, which has facilitated cheaper travel to the region from Western Europe. Therefore, in addition to being an inexpensive destination due to its relatively lower cost of living, Eastern Europe has also proved to be financially attractive to tourists thanks to the lower cost of flights to the region.

For example, Euromonitor International’s research shows that the UK has emerged as the most important source of tourists in the Czech Republic, making up a 7% share of total arrivals in 2003. This translates to an increase of 49,000 more arrivals in 2003 than in 1999. Visitors from the UK were not only attracted to the Czech Republic because their money stretched further, but also to the fall in airfares that has coincided with the arrival of budget airlines.

Consumers can create their own holidays to Eastern Europe

The movement from packaged holidays to tailor-made holidays is also proving to be beneficial to the Eastern European travel industry. Euromonitor’s head of travel and tourism research, Caroline Bremner comments, "At Euromonitor, we have noticed that in recent years there has been a decline in popularity of the traditional packaged holiday concept in favour of consumers booking each element of their holiday separately. Eastern European countries have benefited from this trend with consumers opting for less developed tourist destinations that are still well-served by low-cost airlines."

A positive future for the Eastern European travel industry

Euromonitor International forecasts that the popularity of Eastern Europe is set to continue, predicting growth of 40.2% in incoming tourists to the region between . Key markets to watch include Slovakia and Bulgaria, with Euromonitor also expecting continued rapid growth in Serbia and Montenegro. All three of these countries are set to see a rapid increase in the numbers of arrivals, thanks to further domestic investment in tourism and the appeal and growing availability of low-cost flights.

Euromonitor International’s report, The World Market for Travel and Tourism offers a comprehensive guide to the size and shape of the travel and tourism market at the global and regional level. It examines the size of the travel accommodation, transportation, car rental and retail travel markets, allowing you to identify the sectors driving growth. It identifies the leading companies and offers strategic analysis of key factors influencing the market, including background information on disposable income, annual leave and holiday taking habits.

Euromonitor International, 2004

Lost-cost airlines succeed where communism failed

Anthony Browne

Slovenia, Poland, Estonia and Croatia among the country's opened up by low cost flights

Poland's historic capital, Cracow, was long a beautiful backwater. The stunning medieval buildings could not mask the poverty, and the world largely passed it by.

Then the cheap flights began arriving. First it was Germanwings, flying from Cologne, followed by SkyEurope, easyJet, Ryanair and Centralwings, bringing travellers from across the rich West to Poland’s southern city. There is now a daily flight from Liverpool to Cracow.

Last year three million tourists visited Cracow — 50 per cent up since 2004. Property development has mushroomed, with two new five-star hotels expected this year, and tens of thousands of jobs created.

“The revitalisation is visible. People are happy because they are earning money. The city is looking better,” said Artur Zyrkowski, head of tourism for the city. The low-cost airlines have transformed neighbouring Katowice from grimy post-communist obscurity to another tourist gateway, with a million passengers last year, and a new shopping mall and airport terminal being built.

The low-fare revolution that has swept the airline industry is now sweeping Eastern Europe, integrating the former communist countries into the EU more effectively than any government programme.

Low-cost airlines have been around in Western Europe since deregulation of the skies a decade ago, but they got going in Eastern Europe only after the former communist states joined the EU in 2004.

Jan Skeels, of the European Low Fares Airlines Association, said: “As soon as they joined the EU, they had to adopt EU legislation and open up their skies. Beforehand there was a bit of protectionism. They are a bit further behind — there is still quite a lot of growth in the Eastern market.”

As well as Western low-fare airlines, entrepreneurs in Eastern Europe have been setting up their own operations, such as Hungary’s Wizzair. They are bringing tourists, business people and buyers of second homes east, and entrepreneurs and jobseekers west.

Prague and Budapest may have led the way, but the airlines are spreading their tentacles to ever-remoter destinations. EasyJet last week opened up a route from Luton and Bristol to Rijeka in Croatia.

There plenty of airport sites in Eastern Europe — including disused military bases from the old Warsaw Pact days.

Opening just one route can have an extraordinary impact on a country’s tourism industry. In 2004 easyJet started flying to Ljubljana, the capital of Slovenia, and the number of visitors jumped by 50 per cent in one year.

Towns are seeking a slice of the action, offering marketing deals to get airlines to add them to their list of destinations. Mirabor, Slovenia’s second city, has a campaign to get Ryanair to land. The tourism can give a great boost to the eastern economies. Tallinn, capital of Estonia, has been transformed by the influx of holidaymakers, who exceeded three million in 2004. Helena Tshistova, of the Tallinn tourist board, said: “There are a lot of new hotels and new buildings, new shopping centres and modern buildings in the city centre — and we’ve been renovating the old town.”

The low-cost airlines are also bringing people who are buying second homes. A quarter of a million British families now have properties overseas. Mandy Westmoreland, director of A Place in the World, an estate agent that helps people to find properties overseas, said that the impact of the low-cost airlines was highly significant. “You can go for a weekend in Bratislava or Prague. It used to be just the rich who could afford to go to Paris for a weekend, but now someone on an average income can go to Budapest for a weekend.”

Times Online, 2006

Hungary Tourism Report Q4 2009

Tourism Overview

Based on new data series, and following annual declines in foreign tourist arrivals (defined as nonresidents staying at least one night) in the period 2004 to 2007, BMI estimates that there was a recovery in tourist arrivals last year, edging up a modest 2% year-on-year (y-o-y) to about 9.5mn arrivals. The most recent data are for Q109 and show a moderate increase in foreign visitor arrivals (including sameday visitors), although the number of foreign tourist arrivals has changed little, compared with the corresponding period in 2008. More comprehensive data from the hospitality sector for the first five months of 2009, however, show a sharp downturn in tourism.

Hospitality

After a disappointing year in the hospitality sector in 2008, latest data for the period January-May 2009 confirm a major slowdown. The number of nights spent in all accommodation establishments declined by over 12% y-o-y, with tourist nights accounted for by international visitors falling more than 14% compared with the same period in 2008. Nights by domestic residents also fell by nearly 10% y-o-y. Of the major source markets, the picture is broadly one of negative growth. Tourist nights by German arrivals were down about 14% y-o-y, while nights by Austrian tourists rose by 1.6% y-o-y. The decline in tourist nights by UK visitors continued to be very large, down 33% y-o-y (after major declines at the end of 2008), while nights by Italian tourists fell 3% compared with the corresponding period a year earlier. French tourist nights, meanwhile, were down just 1% y-o-y but nights by visitors from the US declined 34% y-o-y. Unsurprisingly, the average occupancy rate of hotel rooms in the five-month period was also down sharply y-o-y to 37.8%.

Forecast Scenario

BMI forecasts a sizeable fall in foreign tourist arrivals this year. Clearly, recession in Hungary’s main source markets, Romania, Poland, Slovakia and the eurozone (which accounted for around 80% of tourist arrivals in 2008), will have a negative impact on the number foreign tourists in the short term. Moreover, the economic downturn in key markets is also likely to outweigh any benefits to Hungary (for the tourism sector) from further forecast short-term falls in the Hungarian forint against the euro. BMI expects that the number of foreign tourist arrivals will broadly stabilise in 2010, although further weakness is anticipated over the longer term. This is partly due to the forecast strength of the forint (from 2011 onwards) undermining the competitiveness of the tourism sector. In line with our forecast of a deep recession in Hungary in 2009 and economic recovery only in 2011, we foresee negative growth in outbound Hungarian traveller numbers this year, with tourism numbers little changed in 2010 but picking up thereafter.

Business Monitor International, 2009

Asia

Asia Pacific Tourism starts to buckle under pressure

Sian Mannakee

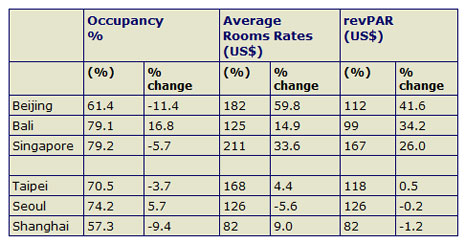

The impact of the current global economic crisis has reached Asia Pacific and the tourism industry is starting to feel the pressure as growth starts to slow. New analysis by Deloitte, the business advisory firm, shows that although hotels have reported positive growth for the year-to-August 2008, with revenue per available room (revPAR) up 13.2%, on closer inspection, hoteliers have started to feel the strain over the last few months.

Until May 2008, revPAR growth across Asia Pacific was reporting double-digit growth each month, with average room rates driving this. However, since then, revPAR growth has fallen back, with June and July reporting increases of 7.5% and 7.4% respectively. Although August bucked this trend, with revPAR posting double-digit growth once more, up 15.2%, this was no doubt impacted by the excellent results Beijing reported after hosting the Beijing 2008 Olympic and Paralympic Games.

This trend is echoed in India which was achieving over 20% revPAR growth at the beginning of the year. RevPAR has dropped progressively each month and is currently in negative territory, down 3.4% during the month of August. On the flip side, Indonesia is one of the only countries bucking this trend achieving double-digit growth each month this year as it continues to recover from the terrorist attacks in Bali during the first half of this decade.

Across the globe, a decline in consumer confidence has meant many people are tightening their purse strings as they have less disposable income to spend on travel and leisure. According to the MasterCard MasterIndex of Consumer Confidence, consumer confidence in Asia Pacific for Q2 2008 was reported at 56.0, compared to 69.3 for the previous period. While these results still show some consumer optimism, the marked downturn will only get worse as the events over the past couple of weeks take their toll. A heady cocktail of the financial crisis, falling equity markets, ,high oil prices and the threat of inflation is taking its toll on corporate travel budgets. This will translate into challenging corporate rate agreements for 2009 which are typically finalised in November. There will inevitably be pressure to reduce room rates.

The International Air Transport Association (IATA) reported that in the month of August alone, airlines in Asia Pacific saw a 3.1% contraction in the number of international passengers, off the back of a 0.5% drop the previous month. These results, coupled with the deceleration in hotel performance across the region, make it clear that economies in Asia Pacific are starting to feel the impact of the wider economic meltdown across the globe.

Commenting, Alex Kyriakidis, Global Managing Partner of Tourism, Hospitality & Leisure at Deloitte said: “Asia Pacific is by no means decoupled from the uncertain and volatile economic environment in the US and Europe, and although the backlash for the Asia region has been delayed, it was inevitable. The collapse of the Asian Stock markets this month will inevitability lead to the same pressures the hotel industry is facing in the USA and Europe where revPAR growth has slowed year-to-August 2008 to 1.0% and 12.6% compared to the same period last year.”

“Looking ahead, the coming months may prove to be a challenging time for hoteliers across Asia Pacific as the economic crisis unfolds. Hoteliers will need to consider how they will respond if occupancy levels fall further. The inclination in tough times is to respond by cutting prices as was the case during the SARS crisis. At that time, like now, the emphasis is on cost reduction while continuing to meet guest expectations.”

The top three and bottom three cities by revPAR growth in Asia Pacific Year-to-August 2008

Survey by Deloitte, 2008

Central and South America

Mark Elliott

Will the real Latin America please step forward – in one corner, political instability, boom and bust economics and severe social problems, in the other, vibrant multi-ethnic cultures, cosmopolitan cities and unrivalled natural beauty. In 2006 the region was finally stepping out of the shadows of 2001-02. With both the Central American (+8.7%) and South American (+8.1%) regions exceeding the global average for tourist arrivals by some distance, the hospitality industry is happy. Investors’ confidence levels are also rising. South American nations are enjoying an influx of capital from Western Europe, while Central America is benefiting from its proximity to the USA, often in the form of large high-end projects such as golf resorts and residences. International hotel chains are also setting up home, with cities such as Buenos Aires, Caracas and Santiago seeing the supply of the four and five-star rooms swell. While no Latin American city makes the top 20 of the revPAR GRI, many cities are climbing back from their post-Millennium lows – as illustrated in the graph below. Only two cities – Santiago and Lima - have overtaken 2000 levels while other cities continue to move up the index. Rio de Janiero leads the region in 61st place, followed by Buenos Aires and Mexico City, at 62nd and 70th place respectively.

Argentina

Good exchange rates and a growth in tourists balanced out Argentina’s relatively minor social problems. Latest results from the World Tourism Organisation (UNWTO) confirm that international tourist arrivals were up 7.6% last year, continuing the upward trend since the political instability of 2002 and devaluation of the Peso. Most visitors come from the USA, Brazil or Chile, but a weak Peso is bringing in more people from the rest of Latin America and marketing aimed at China is widening Argentina’s appeal. With romantic images of Spanish colonial architecture, café culture, and street tango, the vibrant city of Buenos Aires is again capturing the imagination of tourists. In a response to increased demand, the hotel industry is dancing to the same tune. New developments in the four and five-star sector - including those from Hyatt, NH and Sol Melia – are boosting the city’s supply. MICE tourism is seeing strong growth as the government actively promotes this sector. Both average room rates and revPAR are up – 16.2% and 15.6% respectively - although occupancy has fallen slightly.

Brazil

With so much promise, but so many problems, Brazil has yet to fulfil its massive potential as a holiday destination – but there were signs of change in 2006. Stimulated by state investment in infrastructure and incentives targeted at developers, the government tourism body, Embratur, is encouraging hotel investment along Brazil’s north-eastern beach resorts. Embratur has also opened dedicated tourism offices in the US and major European cities in an attempt to drive up international arrivals to Brazil, which has traditionally relied on domestic tourism. While around 65m Brazilians holidayed at home in 2006, just 6m international visitors joined them. The importance of more tourists from overseas is clear – while domestic tourists embrace the low-cost culture initiated by GOL Airlines and Accor’s Formula 1 brand, international visitors are prepared to spend much more. The 6m international tourists spent around US$5 billion in Brazil – the same amount as the 65m domestic tourists. One long-term problem for Brazil has been its lack of air links with Europe, which is reflected in the low number of arrivals last year – 2.5m. However, new direct Lufthansa flights between Munich and Sao Paulo are having an impact. The airline, in combination with Swissair, now offers 19 direct flights to Brazil every week. The carnival capital of the world, Rio de Janeiro, is undoubtedly one of the world’s most beautiful cities. But Rio’s tourism is hampered by its reputation abroad, and the events of 2006 will not have helped. In terms of supply, Rio’s hotel industry remains fairly static. With the Ipanema and Copacabana districts already over-developed, there is little land left for construction. This maybe why average room rates have increased to just over US$155 in 2006, a rise of 12.7% from 2005, in turn driving revPAR. Occupancy levels are static at a little over 60%. The perennial bridesmaid in the battle with Rio for the hearts and minds of international visitors, Sao Paulo, performed well in 2006. Average room rates rose for the third consecutive year, to a five-year peak of US$124. Despite a drop in occupancy, this has boosted revPAR to just over US$74, a rise of 12%. Sao Paulo, as the main financial centre of Brazil and with excellent conference and exhibition facilities, is a magnet for MICE tourism. Although current hotel expansion and construction is dominated by the budget sector, recent openings, including the 123-room Marriott and 310-room Sonesta, have increased supply in the city’s luxury market.

Chile

Chile, the long sliver of land running down South America’s Pacific coast, has continued to punch well above its diminutive stature in 2006. Since the devaluation of the Argentinean Peso in 2002 – which severely dented Chile’s arrival figures – the government, along with the Corporacion Promocion Turistica (CPT) has been improving facilities to attract high-spending visitors. Aided by Chile’s national carrier LAN - the largest airline in Latin America - long haul arrivals from Europe, North America and, more recently, China rocketed to over 2.2m in 2006, according to the UNWTO. Economic stability, security, and a modern tourism infrastructure have all helped, as have Chile’s wide range of products - from ecotourism resorts in Patagonia, to skiing in new luxury centres close to Santiago. As the daily spend of long-haul visitor is nearly three times higher than short-haul, it is understandable that the CPT intend to expand this end of the market. The CPT expected international visitors to have generated around US$1.75 billion last year. As the central gateway city, Santiago is the hub of all Chilean tourism, and an increasingly important business centre. The boom of hotel construction in 2004 and 2005 - when five international brands were opened - created something of a price war. This calmed down in 2006, with average room rates rising to US$104, up 15.1%. Occupancy was up to 68.7% - reflecting Chile’s popularity.

Mexico

Hurricane Wilma wiped out the Gulf coast – the area that brings in 65% of the country’s revenue – and so the ongoing impact is harsh. 2006 was a year of restructuring, and visitor numbers fell by 2.8%. The Economist Intelligence Unit (EIU) estimates that some US$2.7billion has been pledged towards repairing the damage. The bulk of this money has come from private investors, but the Mexican government is putting in $250m. The political climate is stable, as presidential elections have come and gone without the economic shocks that have greeted previous voting, and hotel companies are delighted. Stable relationships with its US neighbour are also valued, as around 85% of visitors to Mexico cross the border from the US. New air routes between the two countries are encouraging more people to pay a visit, with low-cost airline Click Mexicana now flying direct between Cancun and Miami. Mexicana meanwhile has opened a Mexico City-Dallas route. The high-altitude capital of Mexico City enjoyed steady growth throughout 2006. Due to the dominance of business travel, occupancy reached 61.5%. The 0.7% increase in revPAR to US$92 was generated by a rise in average room rates, which now stand at US$149. Recent openings of a Crowne Plaza, NH Hotel and Holiday Inn have brought more rooms onto the market.

Peru

There’s no mystery behind the 2006 success of Peru - this intriguing land of the Incas. The Peruvian government has invested in a programme of sustained promotional activities, focusing on its nature tourism products. The country’s stand at the Hong Kong Travel Expo last year for instance, and an international advertising campaign, have brought in 10.7% more international arrivals. This growth is vital for the country, where tourism is estimated to account for 7.7% of total GDP. Peru’s gateway city, Lima, has performed well. The city has corrected its lack of first-class hotels recently, and the city’s revPAR improved accordingly. An occupancy-driven revPAR rise of 21.1% led to revPAR of US$49.

Summary on Central and South America

The region was set back by the hurricane and ongoing social unrest in some cities can still deter tourists from visiting. But there are some very positive signs. Relative economic stability, strong support from the government, and increased air routes will work together to increase its appeal. The bonus is the fact that many Latin American countries have been added to China’s list of authorised destinations, opening the region to a potentially huge flood of arrivals.

Central and South American cities revPAR Rolling-12 analysis (2001 – 2006)

HotelBenchmark™ Survey by Deloitte