Партнерка на США и Канаду по недвижимости, выплаты в крипто

- 30% recurring commission

- Выплаты в USDT

- Вывод каждую неделю

- Комиссия до 5 лет за каждого referral

To assess the investment strategy of our sample funds, we calculated the internal rate of return (IRR) generated by each deal that included an exit (1,228 deals). For the companies that were still controlled by the funds, we used the end of the period (FY 2007) net asset value. However, the high heterogeneity across the funds in the methods used to compute the net asset value of the companies that were still in the portfolio forced us to focus only on the exit cases.[9]

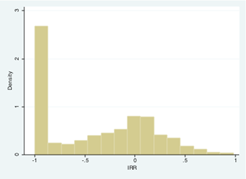

Data on the distribution of the IRRs for the subsample of 1,228 deals reveal that for 31.9% of the exits there was a write-off (IRR=-1), for 32.8% of the exits there was an IRR between -1 and 0, and 35.3% of the exits generated a positive IRR. In 26.4% of the cases the deals generated an IRR higher than the investing fund’s hurdle rate. In the following graph, we report the distribution of IRRs in the sample. Note that the graph does not represent the distribution of the financial performance at the fund level for the analyzed funds because firm performances are not weighted by the size of the investments and because data are censored. In Table 4, we report the incidence of write-offs and of exits with a negative IRR by the level of public ownership in the investing funds.

Graph 1 – Distribution of IRRs for the sample of companies with an exit (1,228 deals)

Table 4 – Incidence of write-offs and of exits with negative IRR for funds with different levels of public ownership

Public share < 50% | Public share > 50% | Public share > 70% | |

Write-off (IRR=-1) | 32.88% | 27.27% | 14.74% |

-1£IRR<0 | 67.22% | 53.11% | 45.26% |

In general, a higher public stake seems to be associated with a lower incidence of write-offs and negative returns. However, this overall evidence might be due to unobserved variables that are correlated with the intensity of public ownership in the investing funds (e. g., size, stage specialization, country/sector focus of the investing funds). Moreover, for a proper interpretation of the data on the incidence of write-off cases, we need to account for the fact that 174 out of 179 funds were still active at the time of data collection. This fact implies a potential censoring effect (i. e., we do not observe the future expected IRRs of the target firms that are still in the portfolios of the investing funds) that can have a relevant and non-obvious impact on the observed incidence of write-offs and negative returns. The empirical analysis presented in Section 5 aims to disentangle these effects through the introduction of appropriate controls, both at the fund and the target company levels.

Concerning fund-level control variables, we used the size of the VC fund, its duration in years, its geographical and stage focus and the hurdle rate. As company-level controls, we included the stage of development of the target companies, their sector and whether they owned patents before the investment of the VC fund. We also controlled for the timing of the VC investment with respect to the residual life of the fund, to capture variations across time in the risk attitude of the fund managers. Because we have a sample of deals across different European countries, we controlled for the state of the stock markets at the time of the investments by including the yearly Morgan Stanley Capital International (MSCI) average stock market index for SMEs. A listing of the variables used in the empirical analysis, along with their definitions and related summary statistics, are provided in Tables 5 and 6.

Table 5 – Variables used in the empirical analysis

Variable | Definition |

Company-level variables | |

WRITE-OFF | Dummy variable that equals 1 for those companies with an exit showing an IRR = –1; 0 otherwise. |

HIGH-TECH | Dummy variable that equals 1 for those companies operating in high-tech sectors; 0 otherwise. |

START-UP | Dummy variable that equals 1 for those companies founded fewer than 6 years before the first investment by the VC fund; 0 otherwise. |

INVESTMENT DURATION | Duration in years from the initial investment to the exit. For the deals without an exit, this measure amounts to the duration in months from the initial investment to December 31, 2007. |

INVESTMENT PERIOD | The timing of the investment with respect to the start date of the fund. The variable is defined as follows: (Date of first investment in company i – start date of the investing fund)/duration in years of the investing fund. The variable consequently ranges from 0 to 1. |

PATENTS | Dummy variable that equals 1 if the target company has been granted patents before the investment. We considered patents granted by the European Patent Office (Source: Thomson Innovation). |

Fund-level variables | |

PUBLIC SHARE | Percentage of public ownership in the investing fund. |

PUBLIC SHARE SQ | Squared value of the percentage of public ownership in the investing fund. |

FUND SIZE | Logarithm of the amount of committed capital in the VC fund. |

SEED FUND | Dummy variable that equals 1 for those funds specializing in seed money; 0 otherwise. |

FUND DURATION | Duration in years of the fund investing in company i. |

HURDLE RATE | Dummy variable that equals 1 for those funds with a hurdle rate higher than 8% (top 25% of the distribution of hurdle rates in the sample); 0 otherwise. |

Market-level variables | |

SME STOCK INDEX | Normalized MSCI average stock market index for SMEs in Europe in the year of the investment in company i. |

Table 6 – Summary statistics for the variables used in the empirical analysis

Variable | Mean | Median | Min | Max | Std. Dev |

WRITE-OFF * | 0.319 | 0 | 0 | 1 | 0.466 |

HIGH-TECH | 0.709 | 1 | 0 | 1 | 0.454 |

START-UP | 0.485 | 0 | 0 | 1 | 0.499 |

INVESTMENT DURATION* | 3.698 | 3.50 | 0.5 | 9 | 1.836 |

INVESTMENT PERIOD | 0.159 | 0.133 | 0 | 0.52 | 0.130 |

PATENTS | 0.289 | 0 | 0 | 1 | 0.453 |

PUBLIC SHARE | 0.278 | 0.190 | 0.012 | 1 | 0.259 |

FUND SIZE | 10.835 | 10.998 | 7.310 | 13.491 | 1.146 |

SEED FUND | 0.048 | 0 | 0 | 1 | 0.215 |

FUND DURATION | 9.59 | 10 | 6 | 17 | 0.030 |

HURDLE RATE | 0.107 | 0 | 0 | 1 | 0.309 |

SME STOCK INDEX | 1.606 | 1.678 | 1.150 | 1.921 | 0.247 |

* Summary statistics include only the companies with an exit.

5. Empirical analysis and results

The empirical analysis is based on two complementary approaches. First, we performed a set of probit models to investigate the impact of the level of public ownership (in the related VC funds) on the probability that a target company results in a write-off. This modeling approach is meant to capture the criteria that underlie the investment selection process by hybrid funds, controlling for contingent factors that are related to the characteristics of target firms, the investing funds and the financial market conditions. Second, we analyzed the impact of the level of public ownership on the duration of the investments through survival models. Following the spillover hypothesis, this latter set of models aims to test whether hybrid funds characterized by a higher public stake show a tendency to postpone the exit of their portfolio companies. In particular, we focused the analysis on cases of exits with intermediate levels of IRRs.

In Table 7, we report the estimates for a set of probit models on the likelihood of write-offs. All of the models are based on the subsample of 1,228 target firms with an exit. The baseline model specifications I and II show that, as expected, the likelihood of a write-off is higher for those companies that are younger, operate in high-tech sectors, or are funded by specialized seed-money VC funds. All else being equal, a higher hurdle rate is associated with a higher probability of write-off, although with limited statistical panies owning patents are less likely to end up being written-off. We cannot find a significant effect for the size of the VC fund on the probability of observing a write-off.

|

Из за большого объема этот материал размещен на нескольких страницах:

1 2 3 4 5 6 7 8 |