Партнерка на США и Канаду по недвижимости, выплаты в крипто

- 30% recurring commission

- Выплаты в USDT

- Вывод каждую неделю

- Комиссия до 5 лет за каждого referral

Transferees may find it difficult to know even what questions to ask, which is why the most common predeparture training takes the form of an informational ch factors as job design, compensation, housing, climate, education, health conditions, home sales, taxes, transport of goods, job upon repatriation, and salary distribution typically come to mind. But such things as the foreign social structure, communications links, kidnapping precautions, and legal advice on the law of domicile art seldom considered before settlement abroad.

FACTORS INFLUENCING THE DEVELOPMENT OF ACCOUNTING AROUND THE WORLD

One of the problems that Daimler-Benz faces is that accounting systems vary around the world. This means that financial statements in France, for example, do not look the same as financial statements in the United States. Some observers argue that this is a minor matter, based in form rather than substance. In fact, however, the substance is also different, such as in Peru, where consolidation of related companies is not allowed; in Sweden, where significant inventory write-downs are allowed; and in France and Germany, where tax accounting and book accounting are essentially the same. These variations put the MNE in a difficult position because it needs to prepare and understand reports generated according to the local accounting standards as well as prepare financial statements consistent with generally accepted accounting principles (GAAP) in the home country in order to generate consolidated financial statements.

One of the problems that Daimler-Benz faces is that accounting systems vary around the world. This means that financial statements in France, for example, do not look the same as financial statements in the United States. Some observers argue that this is a minor matter, based in form rather than substance. In fact, however, the substance is also different, such as in Peru, where consolidation of related companies is not allowed; in Sweden, where significant inventory write-downs are allowed; and in France and Germany, where tax accounting and book accounting are essentially the same. These variations put the MNE in a difficult position because it needs to prepare and understand reports generated according to the local accounting standards as well as prepare financial statements consistent with generally accepted accounting principles (GAAP) in the home country in order to generate consolidated financial statements.

Accounting Objectives

Accounting Objectives

Accounting is basically a process of identifying, recording, and interpreting economic events, and its goals and purposes should be clearly stated in the objectives of any accounting system. The Financial Accounting Standards Board (FASB) in the United States stated that financial reporting should provide information useful in: (1) investment and credit decisions; (2) assessments of cash-flow prospects; and (3) evaluating enterprise resources, claims to those resources, and changes in them.2 The users identified by the board are primarily investors and creditors, although other users might be considered important. The International Accounting Standards Committee (IASC), a multinational standard-setting organization comprised of professional accounting organizations from over 40 countries, includes employees as well as investors and creditors as the critical users. Also named are suppliers, customers, regulatory and taxing authorities, and many others.

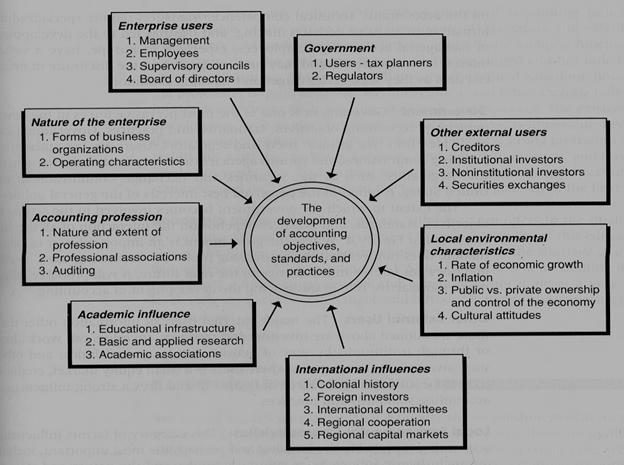

Although the question has been discussed widely, there has been no consensus on whether a uniform set of accounting standards and practices exists for all classes of users worldwide or even for one class of users. To understand the different accounting principles and how they affect the MNEs' operations, we must examine some of the forces leading to the development of accounting principles internationally. Figure 19.4 shows these major factors. The top four factors deal with the nature of the enterprise and the direct users of information. The bottom four represent other major factors that affect accounting objectives, standards, and practices.

Figure 19.4

Major Domestic and Worldwide Factors Influencing the Development of Accounting Objectives, Standards, and Practices

There are several factors that influence the development of accounting objectives, standards, and practices; most of them relate to internal factors, but some of them are a result of external influences. Source: Lee H. Radebaugh,

"Environmental Factors Influencing the Development of Accounting Objectives,

Standards, and Practices—The Peruvian Case," The International Journal of Accounting, Fall 1975, p. 41.

Nature of the Enterprise Within every enterprise there are many users of information, such as managers and employees. The quantity and quality of information provided depends on the users' level of sophistication as well as on the accountants' technical competence. Managers require specialized information to assist in decision making, and this has led to the development of managerial accounting. Employees, especially in Europe, have a vested interest in the enterprise and may have an impact on the disclosure of financial data as they seek better wages and working conditions.

Government Government is one of the most pervasive forces in the development of accounting objectives, standards, and practices. Government can be divided into two groups: users and regulators. Users are tax authorities, planning commissions, and various agencies that compile statistics for general use. Regulators, such as the Securities and Exchange Commission in the United States, respond to the perceived best interests of the general public.

The extent to which the government becomes involved in the setting of objectives, standards, and practices depends on the interaction of all the factors listed in Fig. 19.4. Where the government is an important user of information, does not feel that the accounting profession is meeting users' needs, and does not foresee much change in the near future, it will probably take a much more active role in influencing the development of accounting.

Other External Users The major external users of information other than those mentioned above are investors and creditors. Investors can work alone or through institutions by way of pension funds, mutual funds, and other such investments. In countries where there is a small equity market, creditors tend to be an important source of financing and thus a strong influence on accounting standards and practices.

Local Environmental Characteristics This category of factors influencing accounting is probably the broadest and perhaps the most important, including such diverse influences as cultural attitudes and the nature and state of the economy. The four factors listed in Fig. 19.4 are by no means exhaustive. Although the characteristics are referred to as "local," they are not independent of the world economy. The rates of economic growth and inflation depend on a country's major trading partners as well as on internal economic conditions.

International Influences Many international forces that are institutional rather than environmental have influenced accounting principles worldwide. A prime example is the colonial influence of England and France during the past few centuries. Each of these countries carried their business and accounting philosophies to their colonies and instituted similar systems. The United States also has tended to do this as its economic influence has spread through direct foreign investment.

Accounting Profession As it has done in countries such as the United States, Canada, the United Kingdom, and the Netherlands, the accounting profession itself can influence the development of accounting principles. Three aspects of the profession are important: (1) its nature and extent, (2) the existence of professional associations, and (3) the auditing function. In some countries, the profession is relatively undeveloped and has little influence on accounting. In the United States and the United Kingdom, however, the profession is quite large and well-developed, and it has a strong influence on the development of accounting standards and practices. The existence of associations, such as the American Institute of CPAs, is important, because these groups can often be a force for change. Finally, a strong profession often results in a strong auditing function. Independent external auditors are needed to verify that the financial statements adhere to accepted accounting standards and they represent the true financial position of the firm.

Academic Influence The academic infrastructure refers to the quality of accounting education offered as well as to the accessibility of this education. One of the typical problems in developing countries is the shortage of qualified professors in the accounting field. Since instruction in accounting is not considered a full-time profession and generally is not done at a very high level, little academic research that could introduce change in accounting practices is done.

New words

truck - грузовик

involvement - участие

to wield - орудовать

inherent - неотъемлемый

faith - доверие

advantage - преимущество

expatriates - эмигранты

to complain - жаловаться

to impede - мешать

adjustment - регулирование

reluctant - сопротивляющийся

awareness - осведомленность

to imply - предполагать

approach - подход

workshops - мастерская

assignment - отчисление

tax accounting – налоговый учет

shortage - нехватка

Список использованных источников

John D Daniels,.Lee H. Radebaugh International business/Environments and operations

|

Из за большого объема этот материал размещен на нескольких страницах:

1 2 3 4 5 6 7 8 9 10 11 |